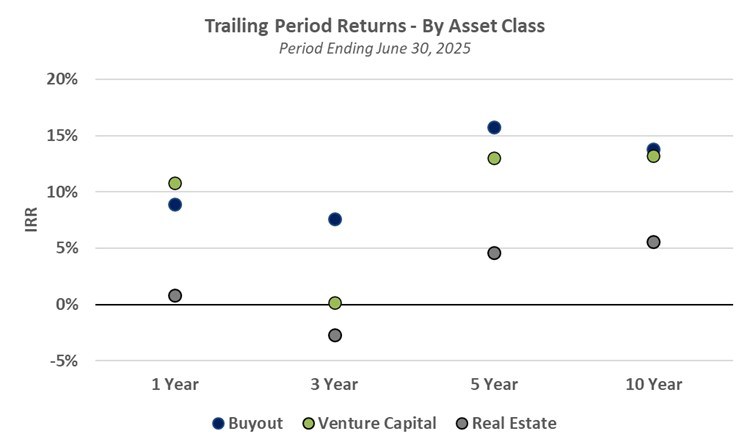

Through the first six months of 2025, private markets continue to produce positive results, albeit paltry in comparison to the broader public equity markets. On a year-to-date basis, based on the quarter ending June 30, 2025, each segment of the private markets posted positive results1 with the best performers buyout, venture capital (particularly late stage focused funds), infrastructure and private credit managers. Real assets (energy, real estate and timber) returns have been lackluster thus far in 2025 as macro headwinds continue to weigh on sentiment for many of the downstream consumers / owners of real estate and natural resources assets. Interestingly, in the near term, European private equity is outperforming the U.S. on a YTD basis by a significant margin (+10.9% in buyout and ~+4.0% in venture capital).

Performance that has continued to trail public equity indices, combined with below average distribution activity, has put further pressure on investors to tighten their belts and only commit to the highest conviction opportunities. However, it is important to remember that successful private markets portfolios require patience and dedication as markets go in cycles. We continue to find interesting opportunities among small company buyout, growth and venture opportunities that we believe are poised to take advantage of long-term opportunities in private markets.

Thematic Insights

Uptick in Distressed & Carve-Out Opportunities

We are starting to see a pickup in the number of distressed / carve-out opportunities within the buyout market. This bodes well for several managers within the Bespoke Private Strategies platform, notably Saothair (focused on the U.S. market) and Endless (focused on the U.K. market).

Saothair, for example, noted at their recent annual meeting that the number of carve-out opportunities is increasing due to several key areas of focus for larger corporations, particularly related to the impact of international tariff impacts and reconfiguration of supply chains.

Growing Concerns in Private Credit

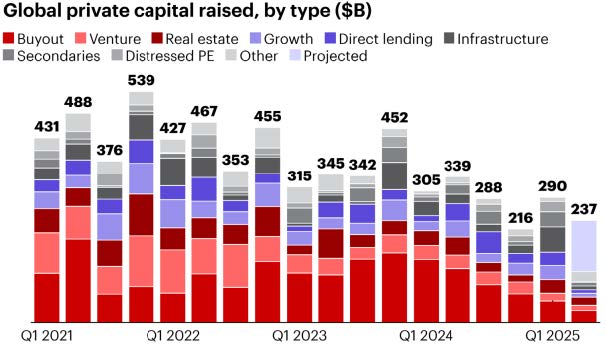

Investors have poured over a trillion dollars into private credit funds1. While they serve a purpose in the lending market, especially as traditional banking institutions are less active providers of debt financing post-GFC, there is a growing concern about the risks and implications of the growth in the private credit market. The risks are exacerbated by a relative lack of transparency and regulation within the non-bank lending space. In fact, many highly regarded investors have recently raised concerns about the private credit market. Among these critics include Jamie Dimon, CEO of JPMorgan, who went on record back in July of this year describing private credit as potentially a “recipe for a financial crisis”2, drawing parallels to the loose lending that preceded the 2008 financial crisis. Jamie Dimon is not alone in voicing his views. Jeffrey Gundlach, CEO of DoubleLine Capital, is also concerned about the private credit market, stating he is “concerned about the industry’s lending practices”3.

Apart from highly selective, opportunistic distressed credit opportunities, we tend not to invest in private credit funds. Fundamentally, we believe the reward is not worth the illiquidity risk in private credit for most of our clients.

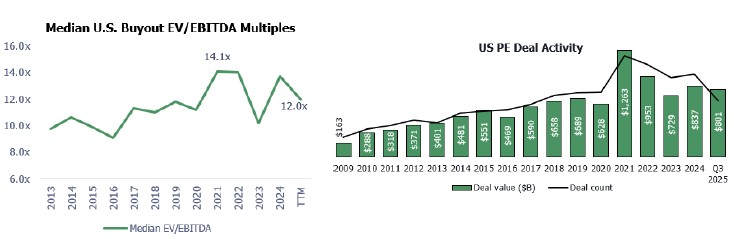

Private Equity Buyout

Based on the most recent data available from PitchBook4, valuation multiples in the U.S. buyout segment remained elevated through the end of 2024. Despite higher valuations, deal activity is up in 2025 as lower borrowing costs are providing some support for new deal activity.

The most challenging issue in private markets remains the lack of liquidity. We said it in our last letter, but it is important enough to repeat: liquidity creates a flywheel effect, providing capital to re-invest which results in improved investor sentiment. Liquidity remains below historical averages, particularly in the more recent vintage years. For fund managers, this situation is creating tension amongst their investors who are increasingly becoming dissatisfied with the lack of liquidity. For some managers, this is beginning to impact their ability to raise fresh capital. For investors, the reduction in liquidity from General Partners is resulting in difficult decisions about re-upping with some managers and heightening concerns about their ability to potentially rebalance portfolios.

On a positive note, Year-Over-Year (“YoY”) growth in revenue and earnings have remained positive through the first three quarters of 2025. Key takeaways at the underlying sector levels include: i) revenue growth in the consumer sector is more muted vs. the prior year and ii) continued resilience seen in the healthcare and technology sectors.

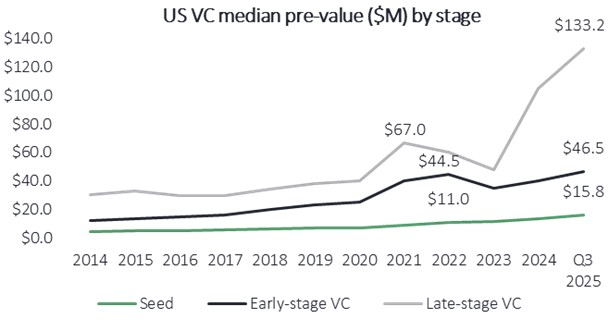

Venture Capital / Growth Equity

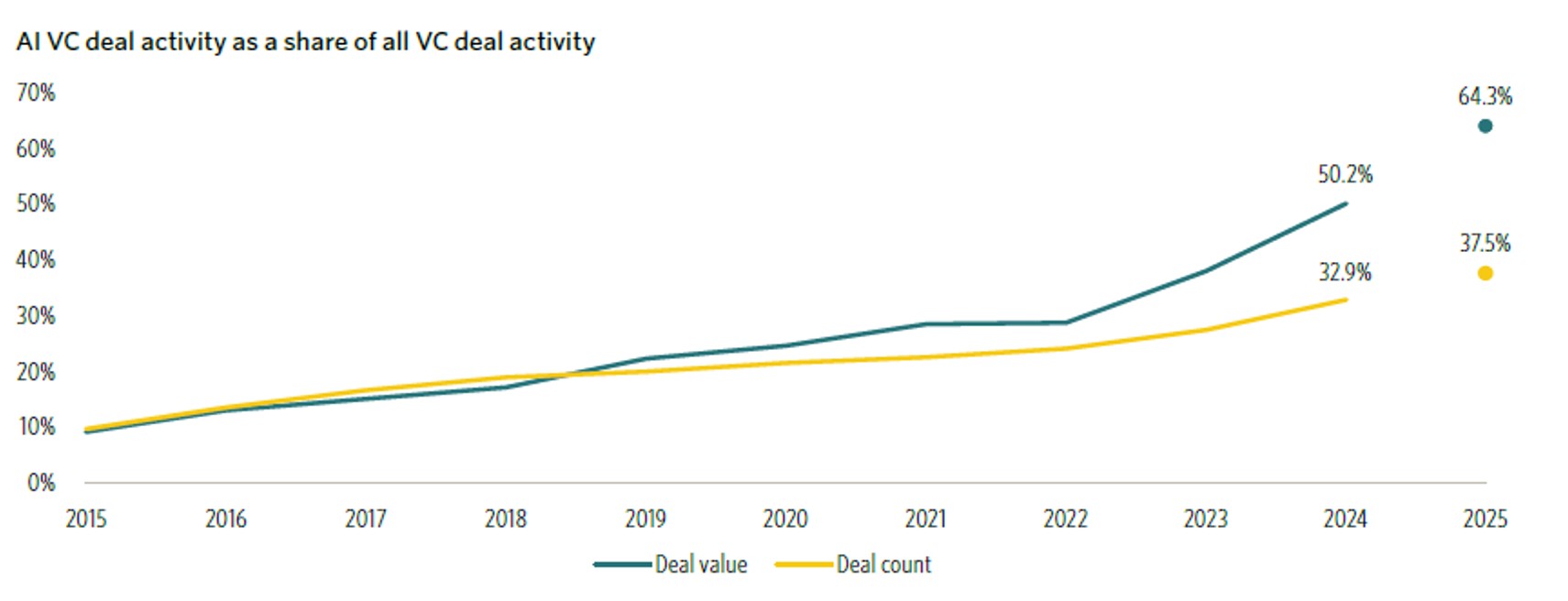

Valuations for early and late-stage VC transactions continue to climb, with the significant increase in the late-stage market being driven by AI companies.

According to research by PitchBook5, “Investor conviction has been increasingly concentrated in AI & machine learning (ML). This sector accounted for 64.3% of venture deal value on a YTD basis, despite representing only 37.5% of deal count”:

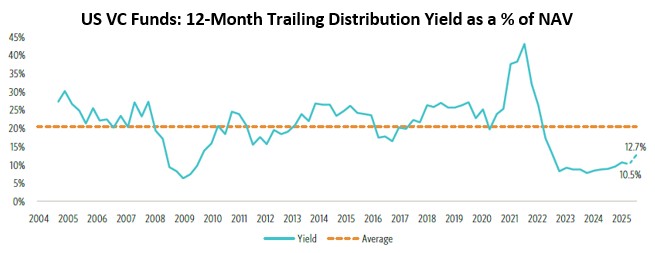

As we have highlighted on several occasions, the lack of general liquidity from venture managers has been a concern of many LPs. As evidenced by the 12-month trailing distribution yield as a percentage of NAV, we are hopeful that the market is showing initial signs of improvement:

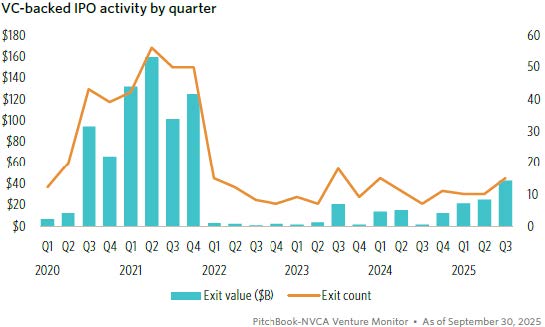

While still relatively low, IPO activity has been showing a little improvement recently. Companies continue to remain private for longer, with PitchBook now estimating that over 40% of unicorns raised their first round of venture capital funding over a decade ago6. If the companies decide to go public, we could see a massive surge in both the IPO count and, more importantly, IPO exit values.

Real Assets

Real Estate

We continue to maintain a fundamentally cautious view on the real estate market and have not actively deployed new capital into real estate assets in over five years. While it is difficult to accurately predict future in capital markets, our fundamentally driven analysis and views on the real estate market have proven to be the right call based on performance results7.

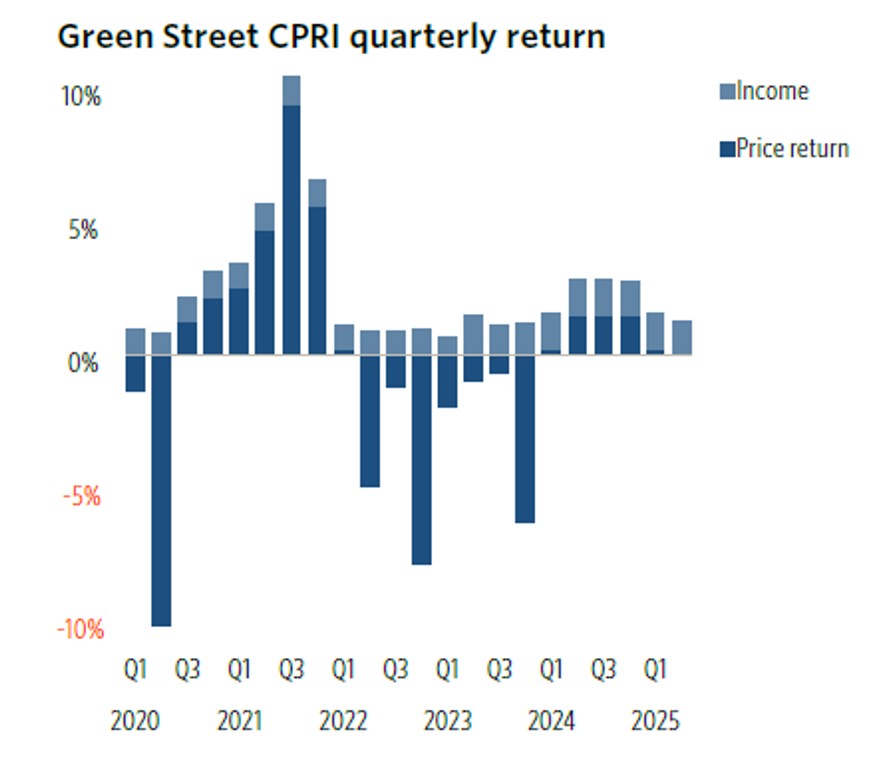

Real estate returns are comprised of two main sources: capital appreciation and income. While the income component is typically stable, capital appreciation is more volatile and can drive ultimate results, especially for value-added and opportunistic strategies. As seen in the chart below8, 2025 may end up being the year of support for North American real estate as prices seemed to find a floor:

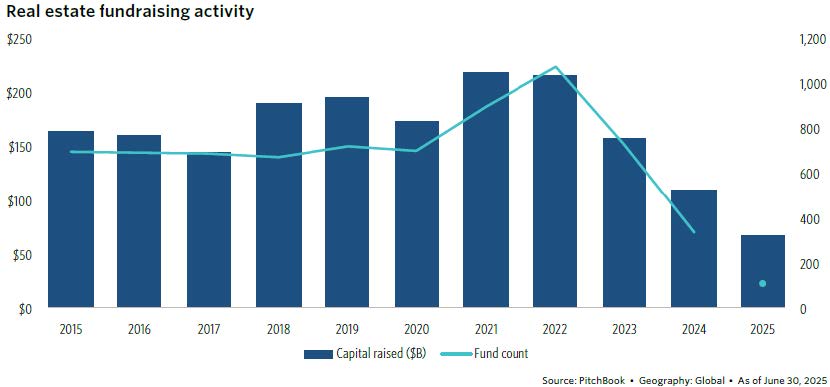

Unfortunately for real estate managers, we have not been alone in our views. According to recent data from PitchBook9, 2025 marks the third consecutive year of a decline in fundraising:

Energy / Natural Resources

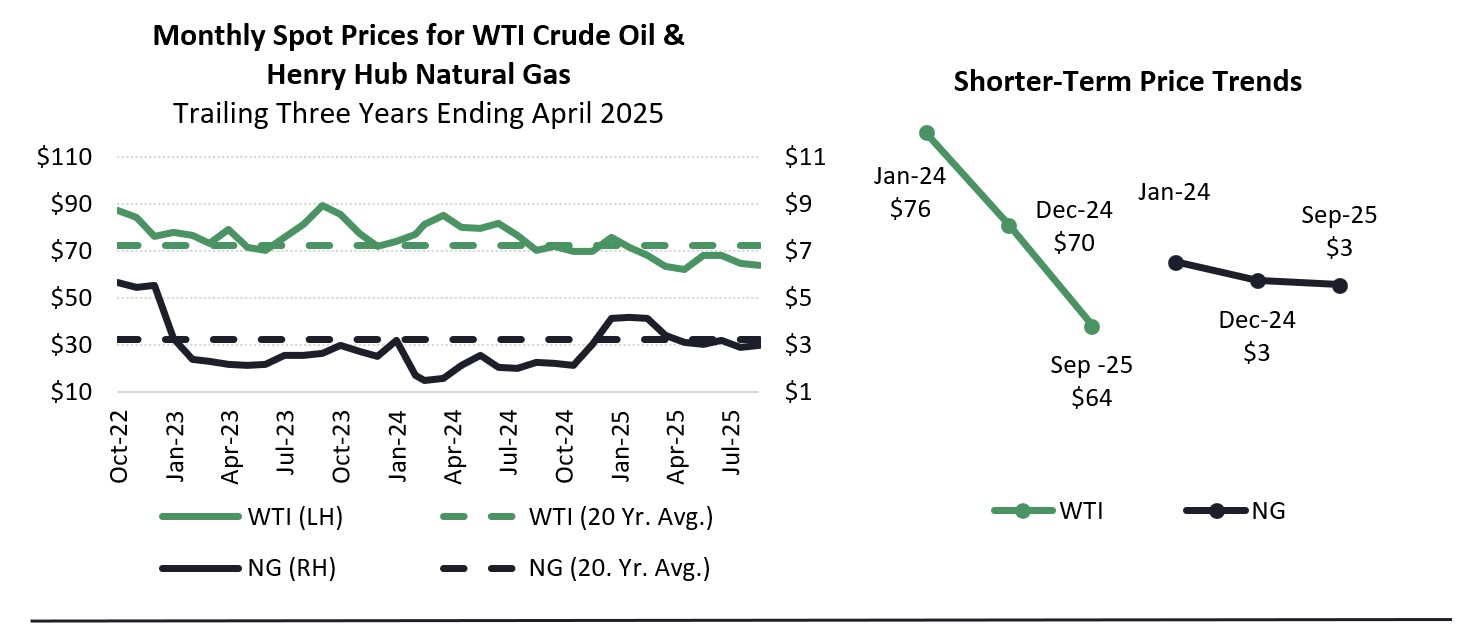

Oil prices were down approximately 9% for the calendar year 2025 through September10, remaining below the 20-year average price per barrel as overall macro-related headlines continued to weigh on the outlook for projected demand and OPEC increased the supply they are providing to the market. After rebounding in late 2024 and into early 2025, driven by a much colder winter, natural gas followed its typical seasonal pattern and, through September, is down approximately 1% for the year.

We hope that this semi-annual letter serves as a helpful reference on the current market conditions and our approach to investing in private markets. Our team members are always available to answer any questions. Thank you for your continued interest and support.

Sources: [1 ] MSCI / Burgiss Private Capital Intel, as of June 30, 2025 [2} https://privatebank.jpmorgan.com/apac/en/insights/markets-and-investing/tmt/private-credit-promising-or-problematic [3] https://www.businessinsider.com/financial-crisis-prediction-private-credit-jeffrey-gundlach-economy-2008-subprime-2025-11 [4] PitchBook: Q2 2025 US PE Breakdown Report [5] Q3 2025 PitchBook-NVCA Venture Monitor [6] Q3 2025 PitchBook NVCA Venture Monitor [7] MSCI/Burgiss Private Capital Intel, as of June 30, 2025 [8] PitchBook H1 2025 Global Real Estate Report, Green Street, As of June 30, 2025 [9] PitchBook H1 2025 Global Real Estate Report [10] U.S. Energy Information Administration

Important Disclosures

This report shall not constitute an offer to sell, or a solicitation of an offer to buy the interests in Bespoke Private Strategies, LP. No such offer or solicitation will be made prior to the delivery of a definitive private placement memorandum, limited partnership agreement and other materials relating to the matters herein. Before making an investment decision with respect to the fund, potential investors are advised to read carefully the confidential private placement memorandum, the limited partnership agreement and the related subscription documents, and to consult with their tax, legal and financial advisors. An investment in any of these limited partnerships is speculative and involves certain risks and conflicts of interest described in more detail in the private placement memorandum. All investments involve risk including the loss of principal or total loss.

Any indices or other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of dividends and other income and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indices have limitations because indices have volatility and other material characteristics that may differ from a hedge fund. Any indices or other financial benchmarks used herein were not selected to represent an appropriate benchmark to compare an investor’s performance, but rather to allow for comparison of the investor’s performance to that of a well-known and widely recognized index.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Lowe, Brockenbrough & Company, Inc. dba Brockenbrough. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Lowe, Brockenbrough & Company, Inc. is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the Lowe, Brockenbrough & Company, Inc.’s current written disclosure statement discussing our advisory services and fees is available upon request.

The opinions expressed are those of Brockenbrough. The opinions referenced are as of the date of publication and are subject to change due to changes in the market of economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed. Brockenbrough is an investment advisor registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Brockenbrough’s investment advisory services can be found in its Form ADV Part 2, which is available upon request.

Semi-Annual Private Investment Commentary