During 2023, investors in private markets experienced a wide array of outcomes largely determined by their respective exposures to different areas of private investments. As the retrenchment in the technology sector continued, those who had larger allocations to venture capital and growth equity funds, in particular, likely experienced relatively lower returns during the year. While performance data for the fourth quarter is not yet fully available, the only segments of private investments that generated positive year-to-date performance through the third quarter of 2023 were strategies focused on generating cash flow yields: mostly private credit and private infrastructure funds.

There have been many discussions on how much deal activity has dropped. With the pace of distributions remaining relatively low, many investors are experiencing negative cash flows (more capital going out than being added back to their portfolios) and finding themselves adjusting their forecasting models.

Thematic Insights

Non-traditional Private Equity Fund Structures

While we are still finding compelling opportunities in traditional limited partnership structures, we have noticed an uptick in the number of high quality, non-traditional structures such as limited liability corporations. While deal structure is important, particularly for investors with tax considerations, our primary objective is finding investment opportunities that are highly accretive, net of all fees and expenses. In today’s environment, we believe our ability to remain flexible and open-minded is paying dividends. The challenge for many investors, particularly large pools of capital, is they often do not have the flexibility to invest in these alternative types of structures. To this end, we are finalizing diligence on a compelling West Coast-based buyout manager with an evergreen fund structure.

Sector Specialists

Our team recently attended an event with approximately 30 highly respected institutional investors, who gathered to share best practices and compelling investment ideas for 2024. While many attendees agreed there is a large degree of uncertainty around various topics such as inflation and the political outlook in the U.S., there was a clear consensus view that sector specialists will continue to have a higher probability of generating outsized returns as compared to generalist firms.

Several research studies have been published that concur with this thesis. One was written back in 2014 by Cambridge Associates, in which it showed that “…investments executed by sector specialists generated an aggregate 2.2x MOIC, handily outperforming generalist investments that generated an aggregate 1.9x MOIC”[1]. A more recent analysis[2] in 2023 from Mantra Investment Partners (“Mantra”) shared the same conclusion. In a related article released earlier this month, Mantra added to their research about the attractiveness of sector specialists with another key attribute[3] : strategies with less than $350 million in assets “…meaningfully outperformed bigger funds”.

Our Bespoke Private Strategies platform has invested in and will continue to invest in sector specialists. We like the fact that their fund sizes tend to be smaller than generalist firms, and the teams are often led by operators who have a high degree of technical knowledge about the industries in which they are investing. All are core fundamental characteristics we seek from prospective managers.

Private Equity Buyout

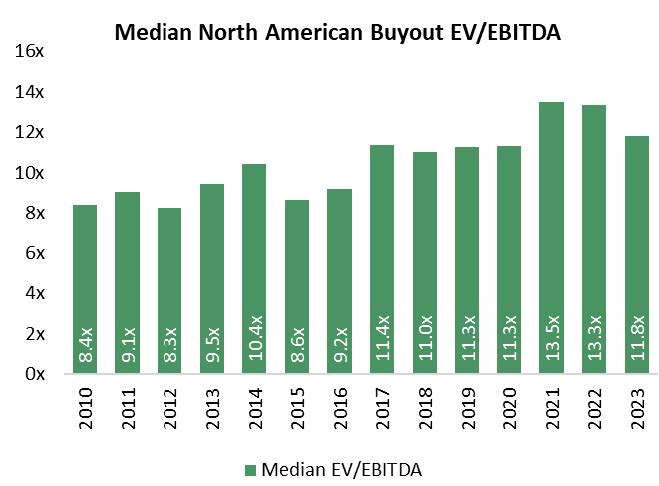

Since valuation multiples tend to be inversely correlated to interest rate moves, multiples have continued to trend down from peak level, albeit perhaps not as fast as some may have predicted.

Source: PitchBook, 2023 Annual US PE Breakdown

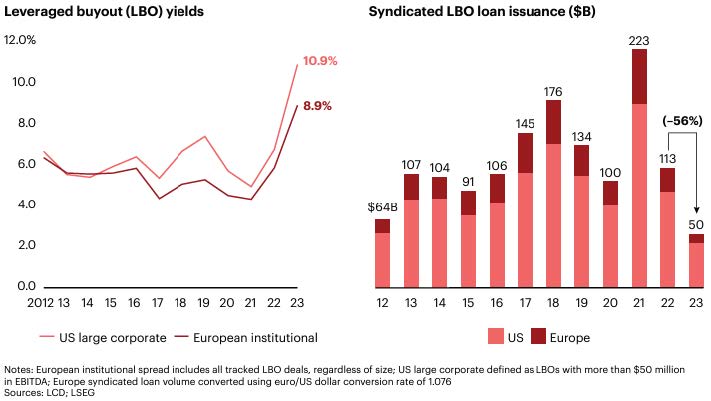

Pressure on multiples is also likely due to the continued, limited exit activity resulting in a relatively small sample of transactions of only the highest quality deals. As seen in the charts below[4], buyout deal activity across the globe dropped significantly in 2023 compared to 2022:

Large / mega buyouts, an area in which we typically do not invest, have been particularly impacted by the current environment. Most often, these transactions are dependent upon a healthy lending market to finance deals. Elevated interest rates and ongoing uncertainty around the outlook for the global economy have put upward pressure on yields for leverage bank loans. In turn, syndicated leveraged buyout (LBO) issuance has dramatically declined.

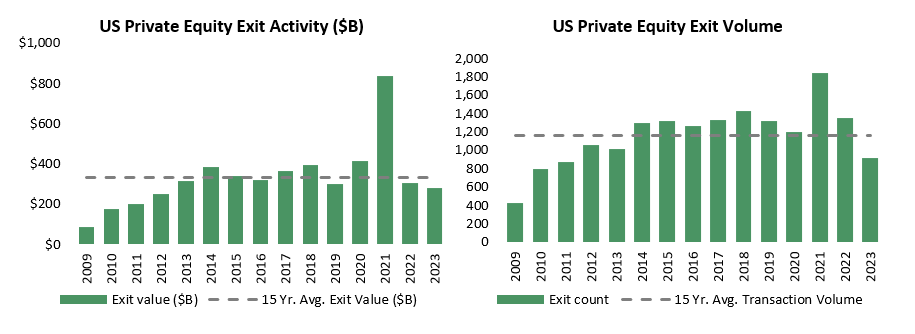

Both in terms of dollar value of total transactions and number of transactions and, exit values were lower in 2023 than both the previous year and each metric’s trailing 15-year averages[5]:

Venture Capital / Growth Equity

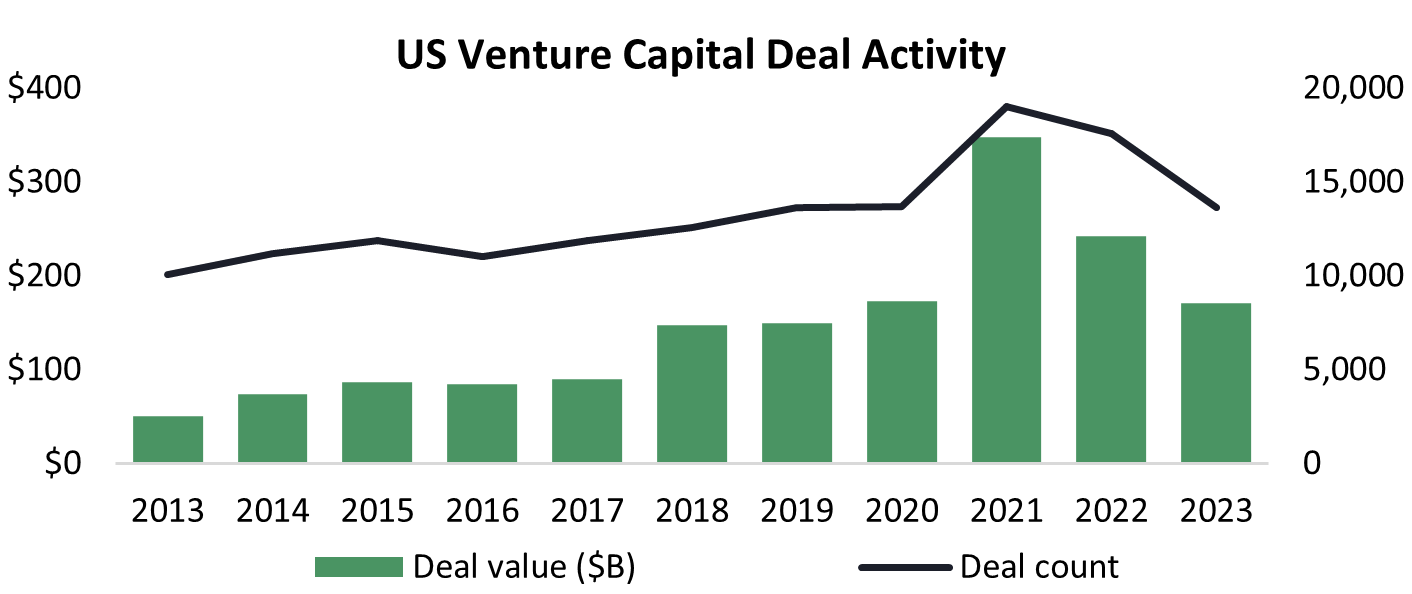

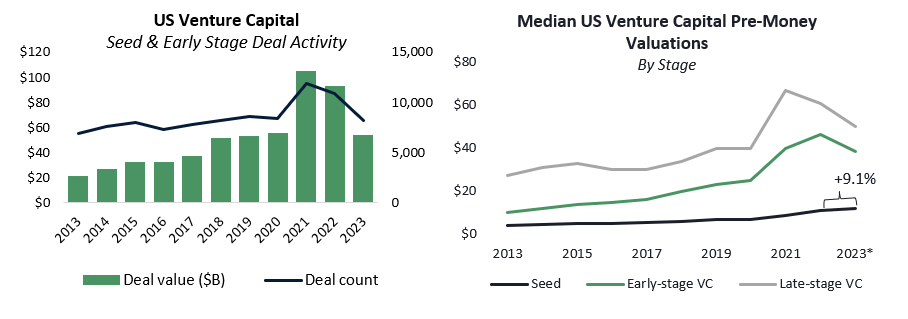

Through year-end, the state of the venture capital market has remained relatively unchanged since our last update. As seen in the following chart[6], deal activity remains below peak levels:

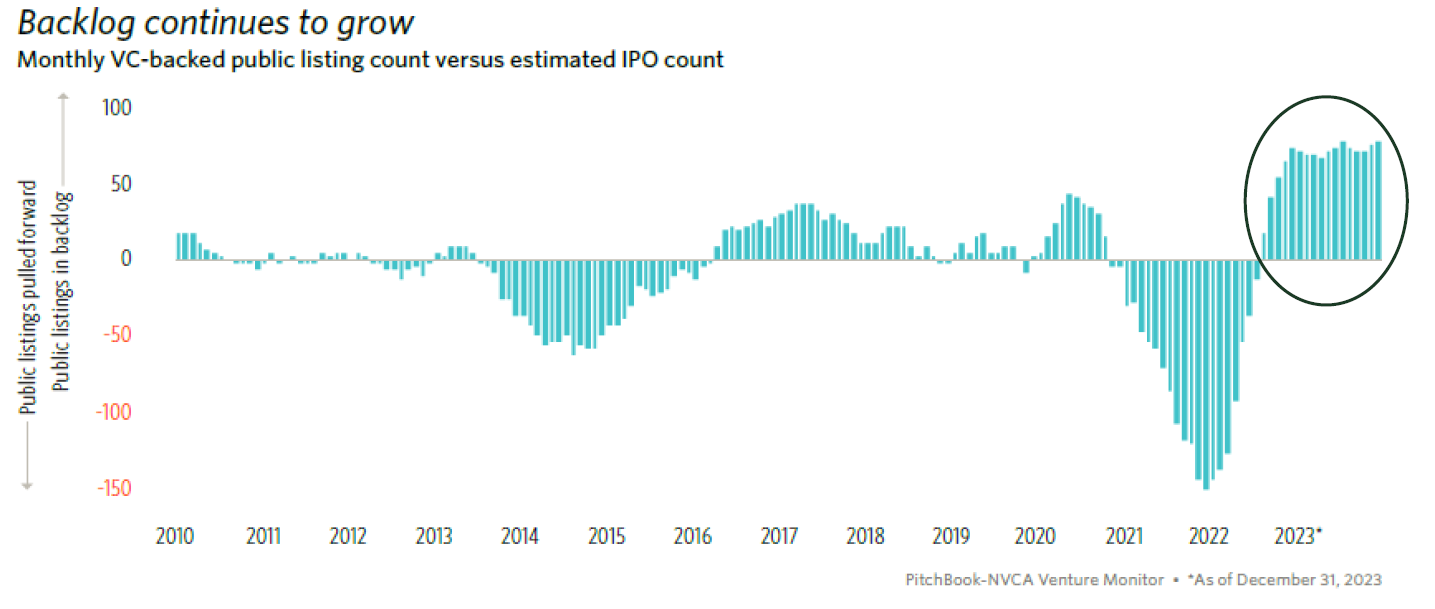

While there were positive signals in 2023 that tailwinds may be returning for VC-backed companies, such as the strong performance in the public markets and a late year jump in the Russell 2000 index, a material recovery has yet to be seen. One driving factor in the recovery for the later stage venture capital market is the IPO market. According to data from PitchBook[7], the excess backlog of companies seeking to go public is at its greatest levels in over a decade:

Similar to the overall market, deal activity in seed and early stage companies was down in 2023. However, for the seed stage deals that were completed during the year, data[7] suggests that investors were willing to continue to support the best founders and pay for this access.

Real Assets

Real Estate

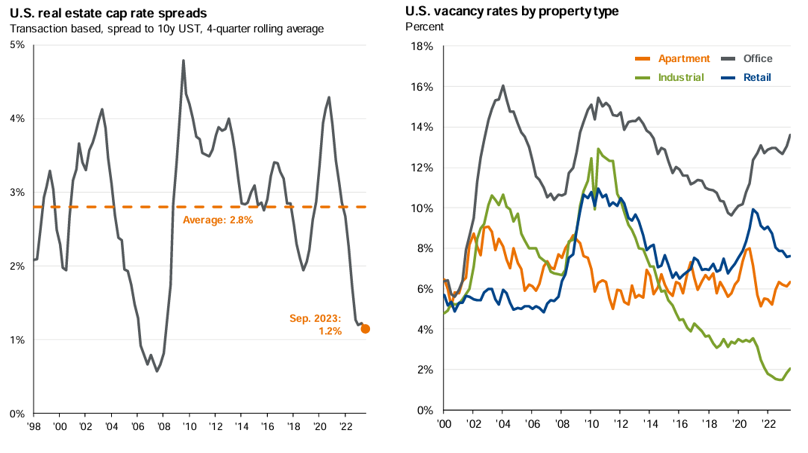

Updated real estate market data[8] below shows the broader real estate market in a continued state of structural pressure, with cap rates remaining compressed. Vacancy rates (mostly driven by supply and demand across sub-markets) in office and industrial properties ticked up further in recent quarters.

Energy / Natural Resources

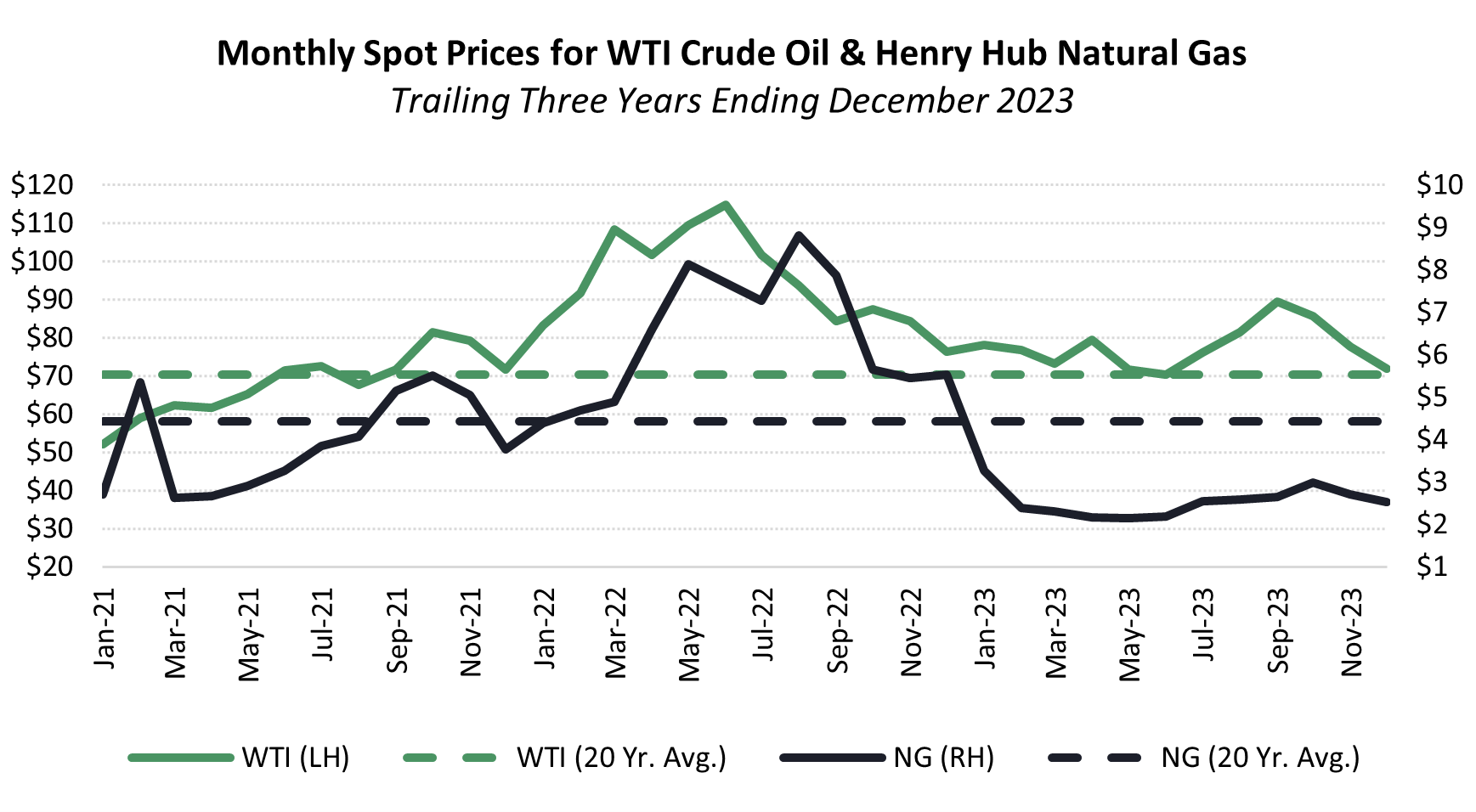

Commodity prices remain in focus for many as they impact inflationary measures and are factored into the Fed’s rate cut decisions. As seen in the following chart, oil prices experienced an approximate 6% decline in 2023[9]. Trending towards its 20-year average price per barrel, oil prices look to be trading in-line with overall supply and demand fundamentals. Natural gas prices, however, continued to free-fall during 2023 as prices were down over 50% for the year. Current excess supply (inventory levels) and estimates for near-term demand (driven by domestic consumption) remain unbalanced and will likely continue keep pressure on natural gas prices.

We hope that this semi-annual letter serves as a helpful reference on the current market conditions and our approach to investing in private markets. Once we have final valuations for the fourth quarter, we will provide an update on each vintage year and the overall the Bespoke Private Strategies platform. Our team members are always available to answer any questions. Thank you for your continued interest and support.

Sources: [1 ] Cambridge Associates: Declaring a Major: Sector-Focused Private Investment Funds [2] Institutional Investor: Small, Esoteric Private Equity Strategies Keep Crushing It [3] Mantra Investment Partners: The Best-Performing Private Equity Funds Share These Two Attributes [4] Bain & Company: Global Private Equity Report 2024 [5] PitchBook: 2023 Annual US PE Breakdown [6] PitchBook-NVCA Venture Capital Monitor, Q4 2023 [7] PitchBook-NVCA Venture Capital Monitor, Q4 2023 [8] NCREIF, NAREIT, Statista, JP Morgan; Vacancy data as of Sep. 30, 2023; other data as of Dec. 31, 2023 [9] U.S. Energy Information Administration

Important Disclosures

This report shall not constitute an offer to sell, or a solicitation of an offer to buy the interests in Bespoke Private Strategies, LP. No such offer or solicitation will be made prior to the delivery of a definitive private placement memorandum, limited partnership agreement and other materials relating to the matters herein. Before making an investment decision with respect to the fund, potential investors are advised to read carefully the confidential private placement memorandum, the limited partnership agreement and the related subscription documents, and to consult with their tax, legal and financial advisors. An investment in any of these limited partnerships is speculative and involves certain risks and conflicts of interest described in more detail in the private placement memorandum. All investments involve risk including the loss of principal or total loss.

Any indices or other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of dividends and other income and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indices have limitations because indices have volatility and other material characteristics that may differ from a hedge fund. Any indices or other financial benchmarks used herein were not selected to represent an appropriate benchmark to compare an investor’s performance, but rather to allow for comparison of the investor’s performance to that of a well-known and widely recognized index.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Lowe, Brockenbrough & Company, Inc. dba Brockenbrough. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Lowe, Brockenbrough & Company, Inc. is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the Lowe, Brockenbrough & Company, Inc.’s current written disclosure statement discussing our advisory services and fees is available upon request.

The opinions expressed are those of Brockenbrough. The opinions referenced are as of the date of publication and are subject to change due to changes in the market of economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed. Brockenbrough is an investment advisor registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Brockenbrough’s investment advisory services can be found in its Form ADV Part 2, which is available upon request.

Semi-Annual Private Investment Commentary