It is no secret that investors in the public markets are experiencing a corrective bear market. Private markets are not immune from the ancillary impacts of negative performance in the public markets, however, there it often takes several quarters for the impact to be reflected. Managers who are patient and prudent during periods of market dislocation are often able to deploy capital into attractive opportunities, whether it be in new companies or gaining increased ownership in existing portfolio companies.

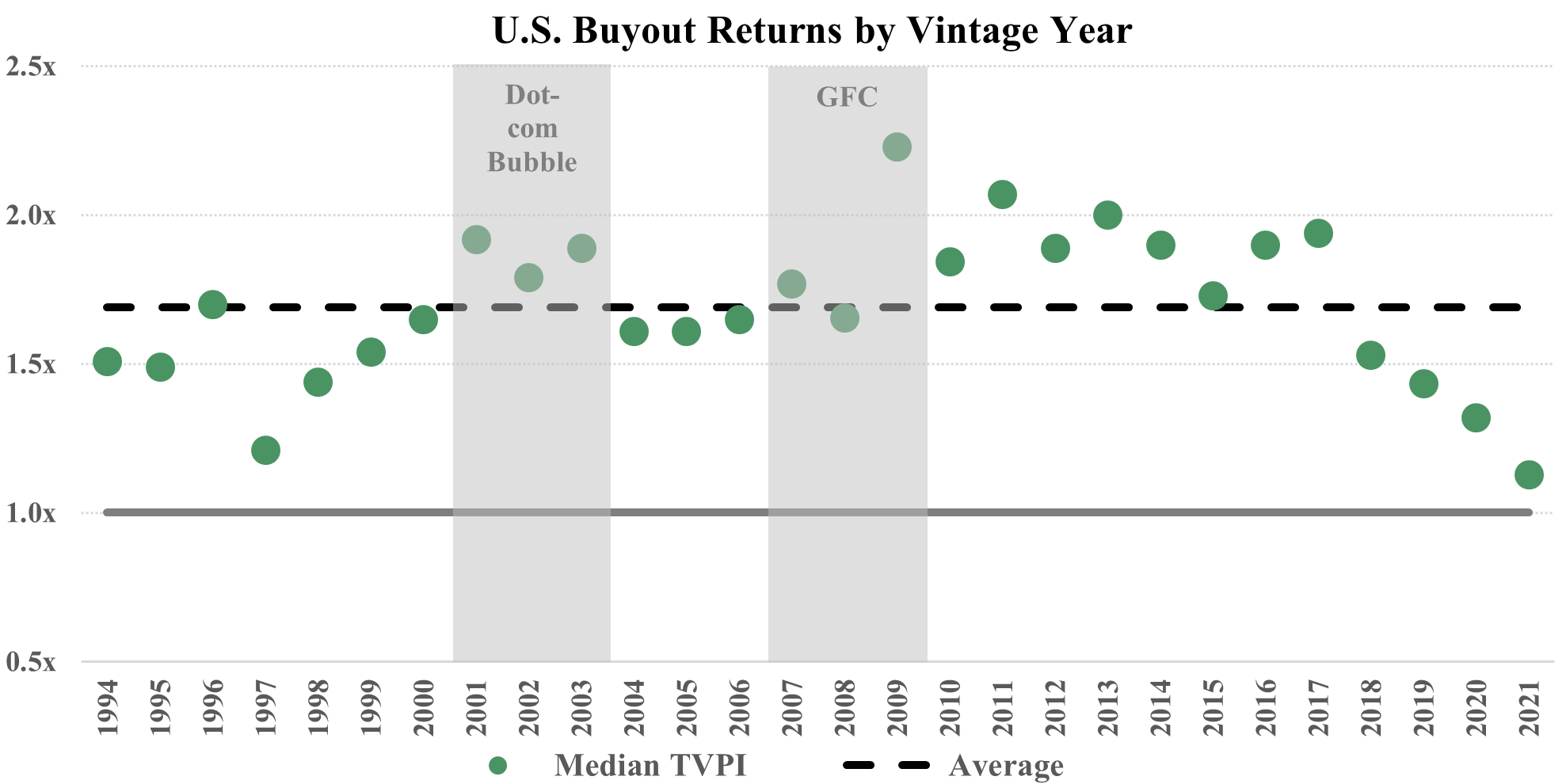

The ultimate impact of a downturn is also often dependent upon underlying exposures to the various private market asset classes. This is partly why we are believers in concentrated, yet well-diversified portfolios across multiple vintage years. A commitment to a long-term approach is critically important to building and managing a portfolio of private investment funds. While history is not always repeated, there is concrete empirical data[1] proving that many of the best performing vintage years in private investments are established in and around recessionary periods.

Thematic Insights

Private Investment Cash Flow Planning in Times of Uncertainty

We often use this section of the letter to highlight specific, more thematic areas of the market. Given the backdrop of the market situation, we thought it would also be useful to revisit the topic of cash flow planning. For some investors, particularly those with regular liquidity needs, cash flow planning becomes an increasingly important consideration during times of economic distress.

While we often see a reduction in capital call activity during a recessionary period, there is a period of a couple of quarters of normalized activity before a drop‐off is experienced. Distribution rates often slow relatively quicker, sometimes drying up almost immediately. This can be due to a widening bid/ask spread among buyers and sellers and a general lack of financing to complete transactions as traditional financiers pull back, both of which lead to extended holding periods for assets. Taken altogether, net cash flows (distributions minus capital calls) for investors in private investment assets are frequently negative during economic downturns.

Distressed Investing

Timing pure distressed strategies is extremely difficult, particularly in a private investment fund structure, because you typically need to commit to the strategy ahead of a crisis, not knowing if the capital will actually ever be fully drawn. We have seen such a scenario play out, both in the Global Financial Crisis (particularly European distressed funds) and more recently during the COVID-19 crash back in early 2020. Whether or not we are entering the next distressed cycle, what is almost a certainty is there will be a number of funds raised purely to focus on acquiring distressed companies/assets.

To clarify, distressed investing has the opportunity to generate very attractive returns. Rather than locking up our clients’ capital in strategies highly dependent upon the characteristics previously mentioned, our preference is to invest in strategies special situations and turnaround strategies. These strategies can be considered a sub-set of distressed investing, yet they generally consist of finding investment opportunities where underlying assets are discounted due to illiquidity, market disruption, business cyclicality or an unsustainable capital structure. In what are highly structured transactions, managers will structure deals with a combination of debt-like downside protection with the potential for equity-like upside. The ultimate outcome is highly dependent upon the manager's experience, expertise, and resources to drive value creation rather than getting lucky at timing the entry point based on the distressed cycle. Importantly, special situations and turnaround managers provide opportunities to perform, regardless of the cycle, and focus on fundamentally good businesses with good assets. Most of these managers shy away from flawed business models with poor products/services.

Private Equity Buyout

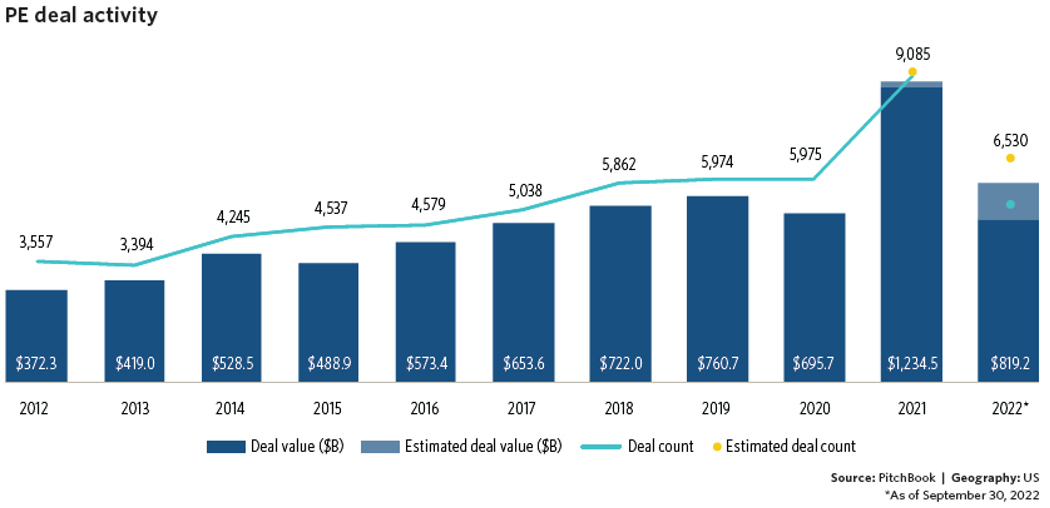

After a record-setting year in 2021, deal activity thus far in 2022 has been muted. This is largely due to rising rates and the associated economic uncertainty brought on by global conflicts and inflationary pressures. As seen in the adjacent chart, deal activity compared to years excluding 2021 is still relatively high:

We are seeing particular pressure in leveraged buyouts where loan volume deceleration is being driven by much more expensive debt in 2022’s market. According to data from PitchBook[2]: “Floating rates for loans on leveraged buyouts averaged 4.8% in February before doubling to 9.8% in September.” In order to balance increased interest costs, some buyers must consider using more equity to complete a transaction. Ultimately, this must be factored into underwriting projections and a determination must be made as to what the projected equity value must be worth in order to achieve the required returns of the deal. This has certainly become more difficult in 2022 to accurately analyze.

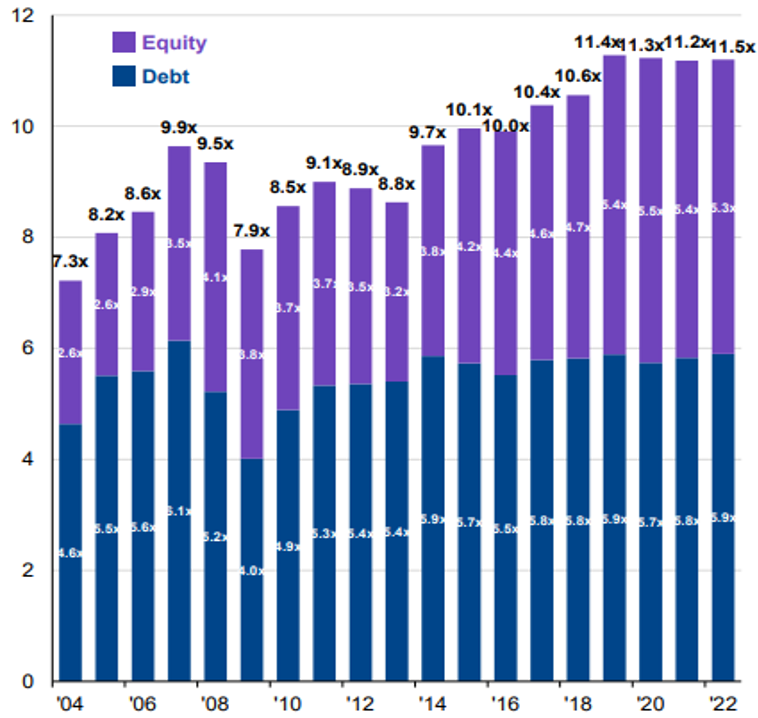

Despite overall pressures on the private equity market, buyout multiples surprisingly continue to show resiliency and remain at relatively high levels, and there remains a strong investor appetite.

YTD 2022 data is showing a potentially smaller amount of capital being raised by buyout managers. Fundraising processes are often closed in certain parts of the year; therefore, it is a difficult measure to project on an intra-year basis.

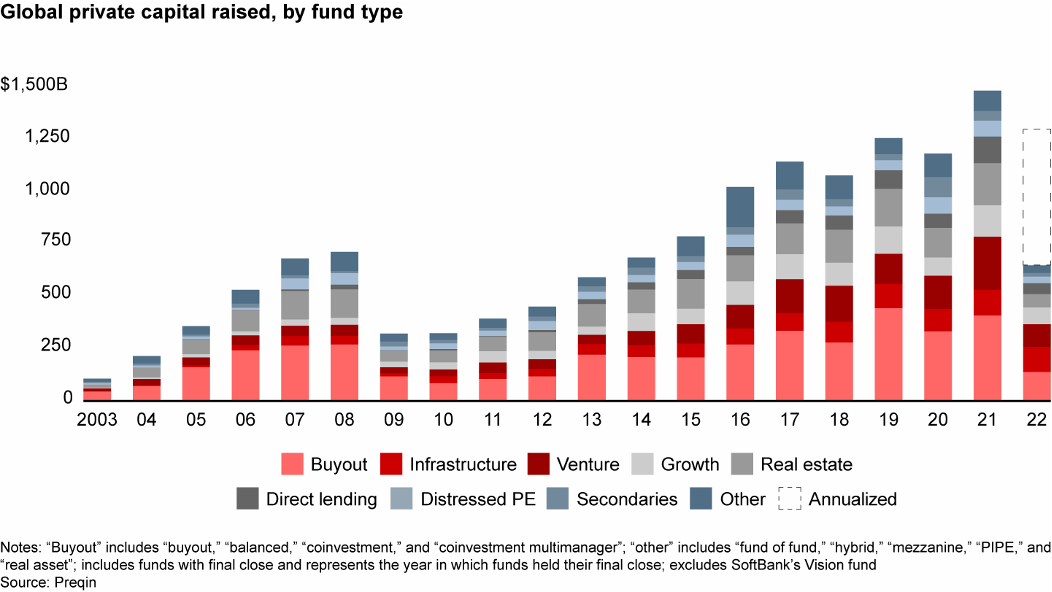

While the overall amount of global private capital dry powder has continued to increase YoY, an interesting trend to monitor is how this impacts the amount of dry powder available to buyout managers.

It’s too early to tell, but this could be the early signs of a slowdown in fundraising in the broader buyout market. This is a likely scenario as LPs are facing a similar denominator effect last seen during the Global Financial Crisis. This could also be a healthy trend for the buyout segment as reduced dry powder could help provide better balanced, competitive dynamics relative to recent periods where continue upward pressures on bids often led to unreasonable valuations. If the pendulum swings too far, a significant reduction in dry powder available to purchase assets can often lead to downward pressure on exit values as capital available to buyers becomes scarce.

Venture Capital / Growth Equity

Through the second quarter of 2022, data from PitchBook shows there has still yet to be any significant uptick in down rounds[3] (defined as a subsequent fundraising round completed at a lower valuation than the previous round). It is important to add context that the sample size is not as large. The number of rounds completed thus far in 2022 stood at 1,370, compared to 3,776 for the entire year of 2021. Annualized, the 2022 figure is approximately 27% below the level set in 2021. Eventually, as companies that need follow-on financings come back to market, we may see the number of flat or down rounds begin to increase. Ultimately, this becomes an exercise in duration and ultimately cash burn management.

Data from Carta[4] is showing signs of compression in valuations for early stage transactions. One exception is seed stage deals, which have continued to modestly increase. Late stage valuations for new transactions, while continuing to see pressure relative to 2021, are surprisingly holding up relatively well. Most of the revaluations we are seeing pertain to assets still held and where managers are taking discretionary write-downs.

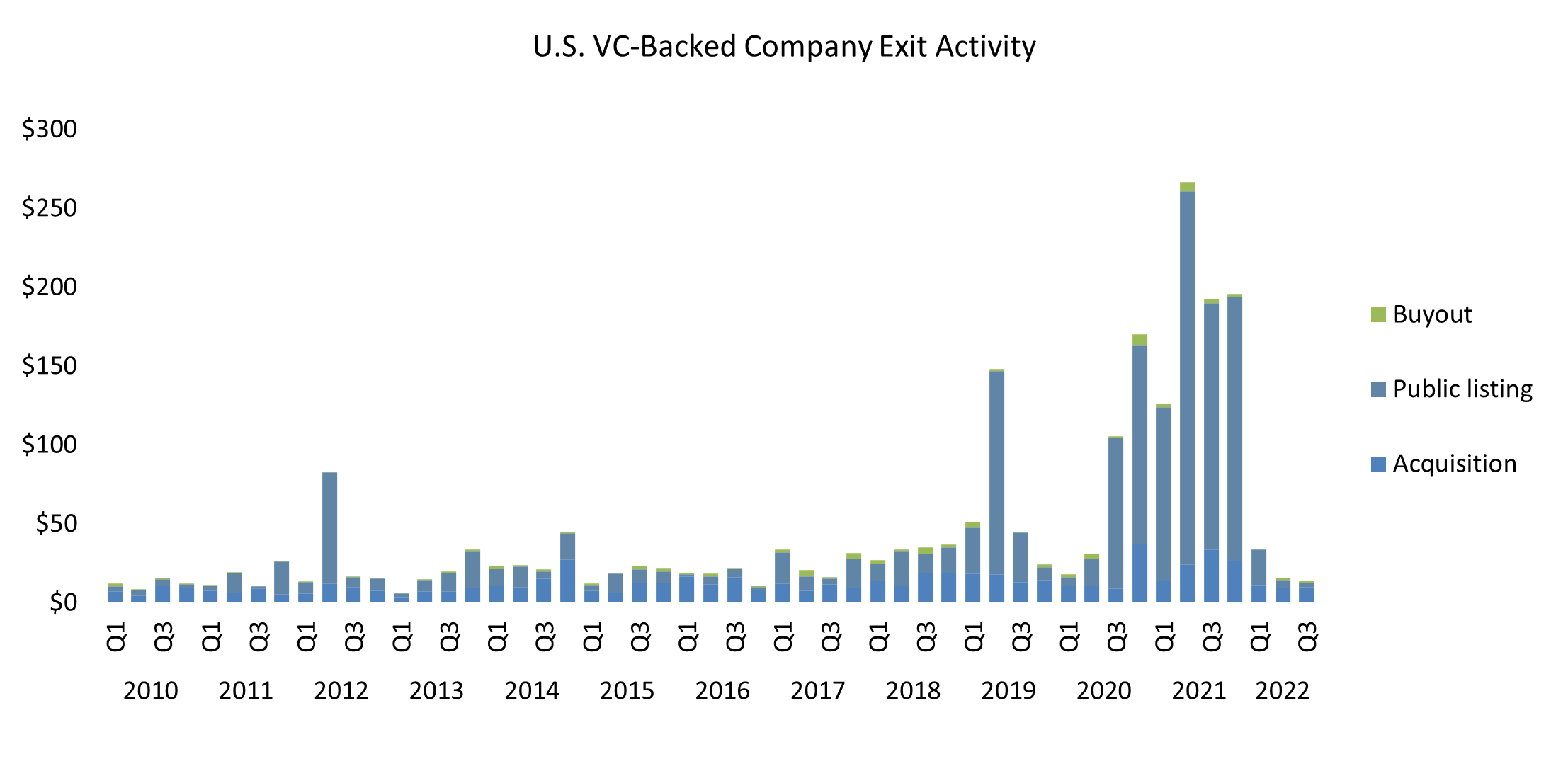

Updated data through September 30, 2022, shows a significant drop in exit activity so far in 2022[5], with the IPO market essentially shut:

With little exit activity, this data is likely congruent with the views that re-valuations are mostly being seen in currently held assets as mentioned above.

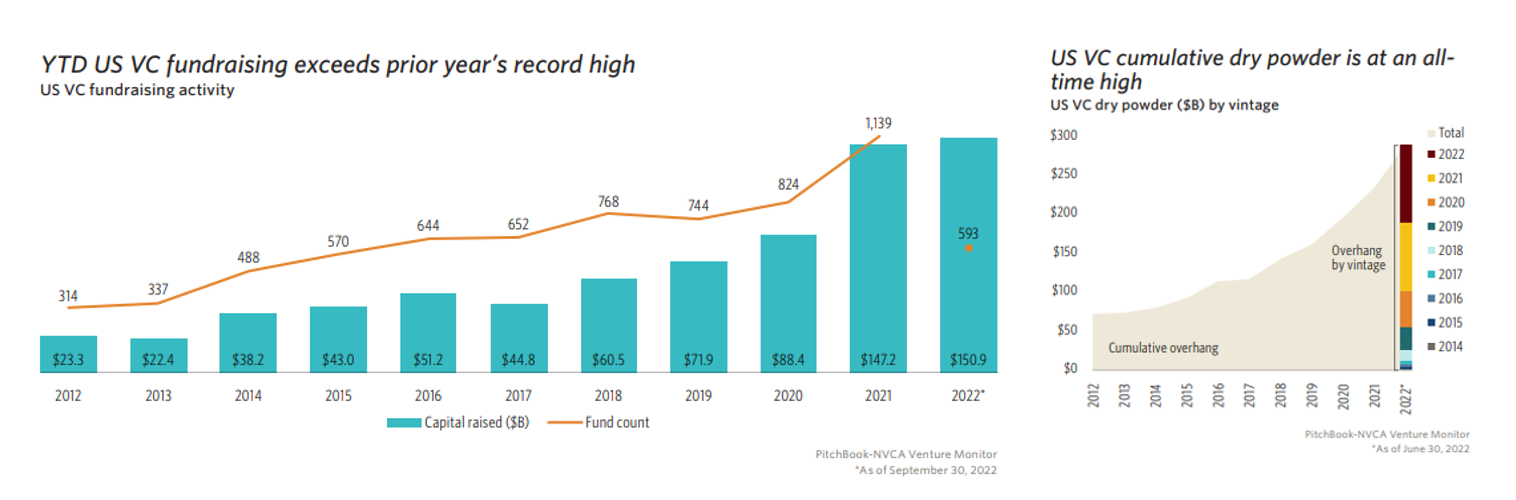

One area that is slightly more optimistic and supportive of the notion that the re-valuations may not be as severe as they otherwise may be is the fundraising market. Fundraising for venture capital funds continues to remain strong thus far in 2022. This, coupled with record amounts of dry powder, is supportive for venture capital companies seeking to raise capital.

Real Assets

Real Estate

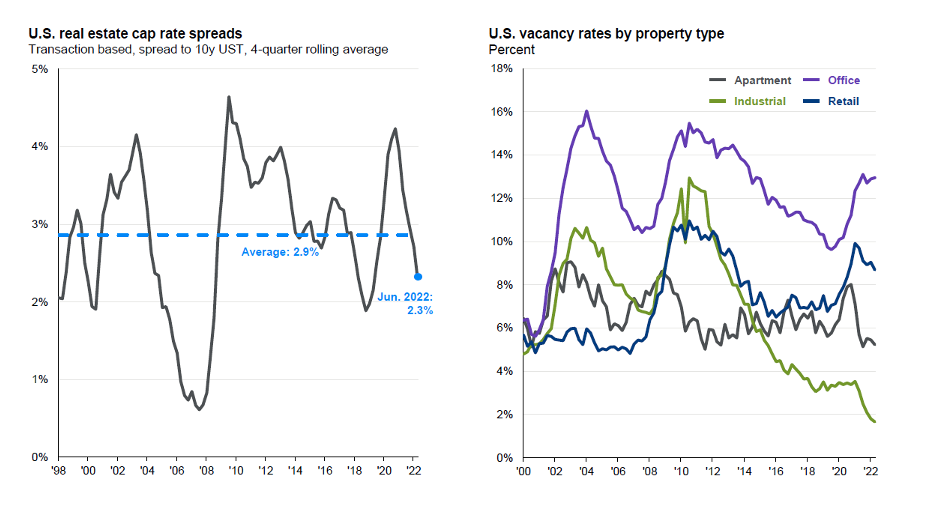

The Real Estate market continues to face pressures on vacancy rates (particularly in office properties) and rising interest rates have impacted parts of the market. We continue to see bond yields rise, and cap rate spreads push below their historical average[6]:

The spread between cap rates and the 10-year Treasury rate does not always move in complete lock-step. Cap rates do not include the cost of a property’s mortgage but rather assumes the property is purchased with cash. Therefore, rising borrowing costs do not directly impact cap rates. It remains important to focus on the three key drivers: gross income, expenses, and transaction prices. An important metric to track is rent growth, which has continued to remain strong across office, retail, and industrial properties[7].

Energy / Natural Resources

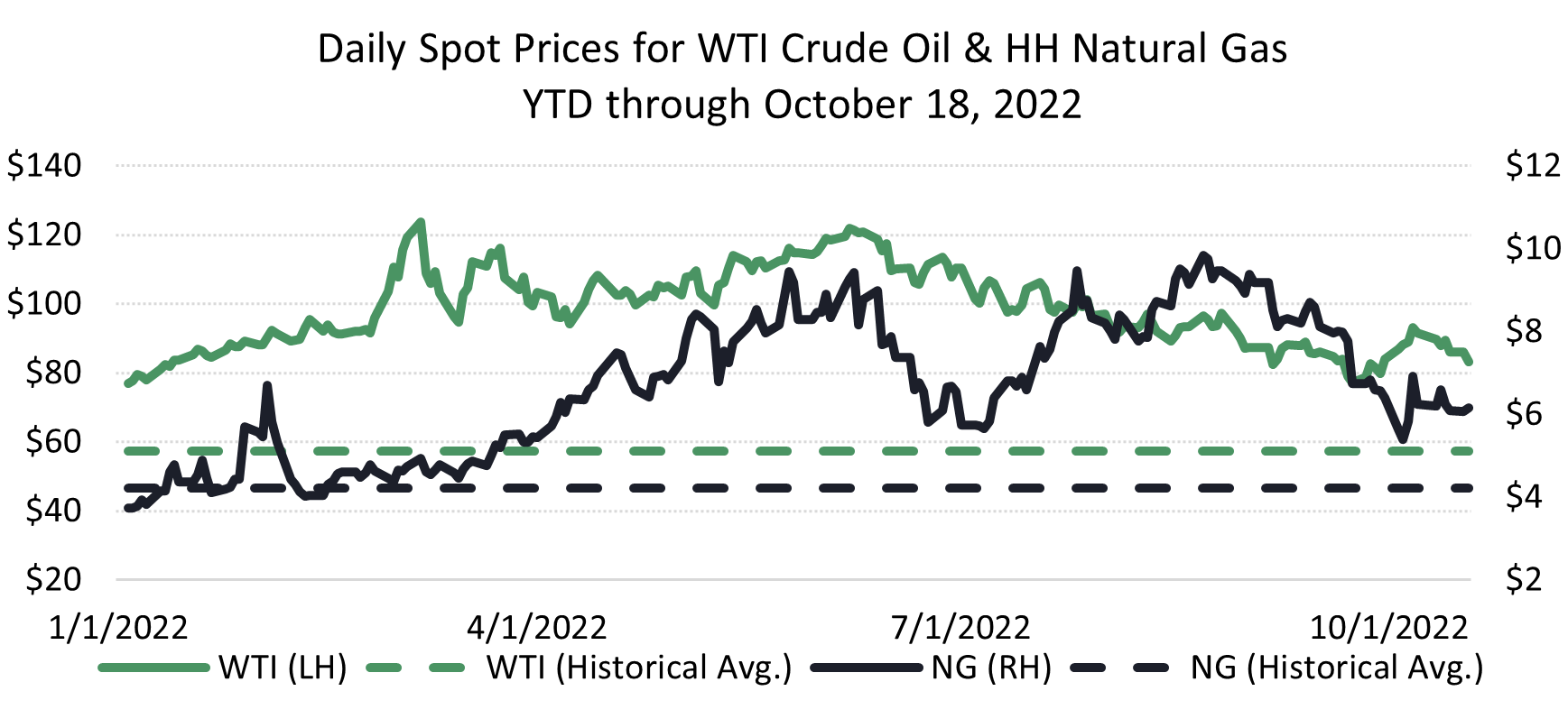

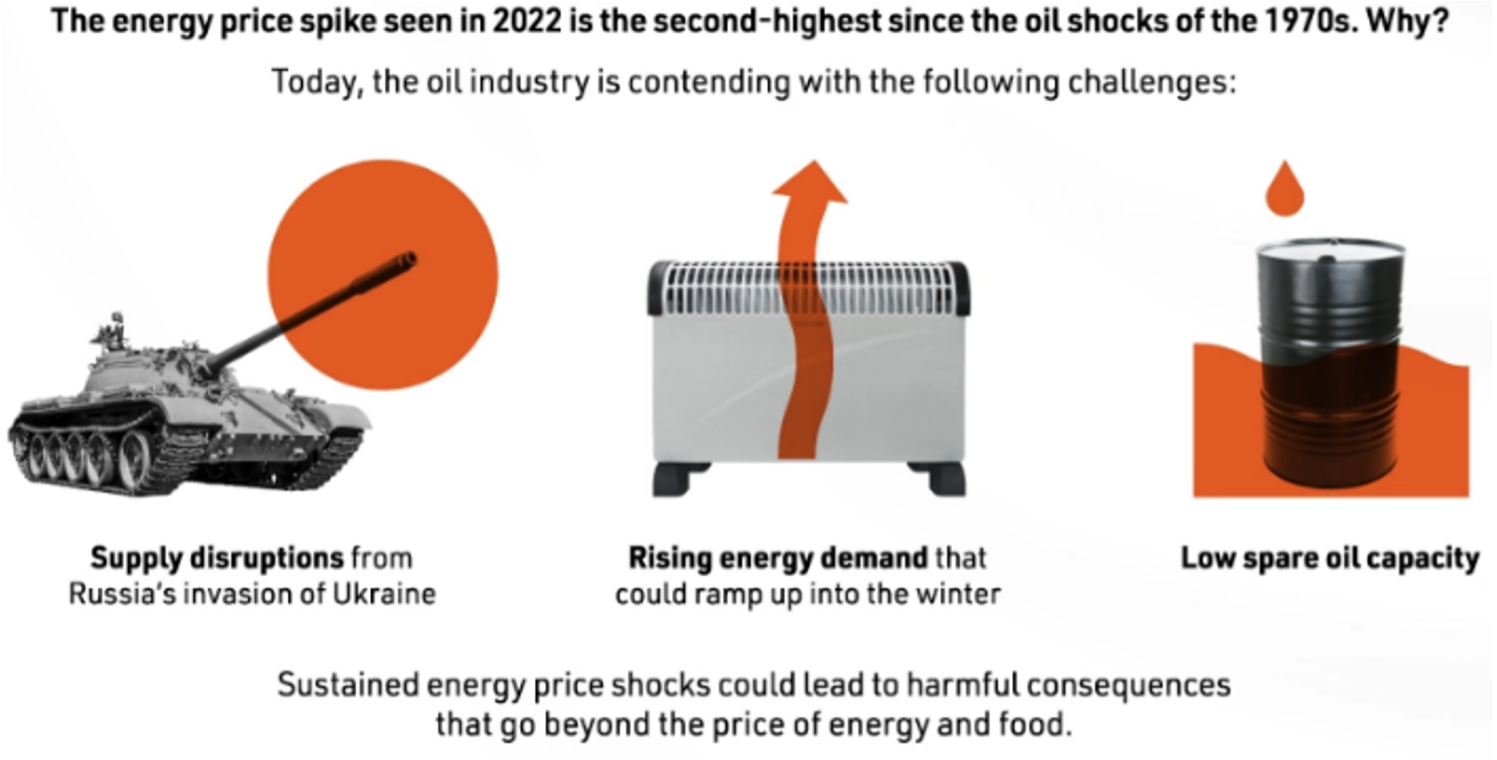

Energy commodity prices have trended down thus far in the second half of 2022 but remain positive on a YTD basis. With continued geopolitical tensions between Russia and the Ukraine and uncertainty around inflation and the resulting measures being taken by the Fed, it may not come as a surprise that crude oil and natural gas prices have been quite volatile[8].

One challenge for companies in a highly volatile market is managing hedging policies and procedures. Most energy producers have active hedging programs in place, at least for a portion of their forecasted production.

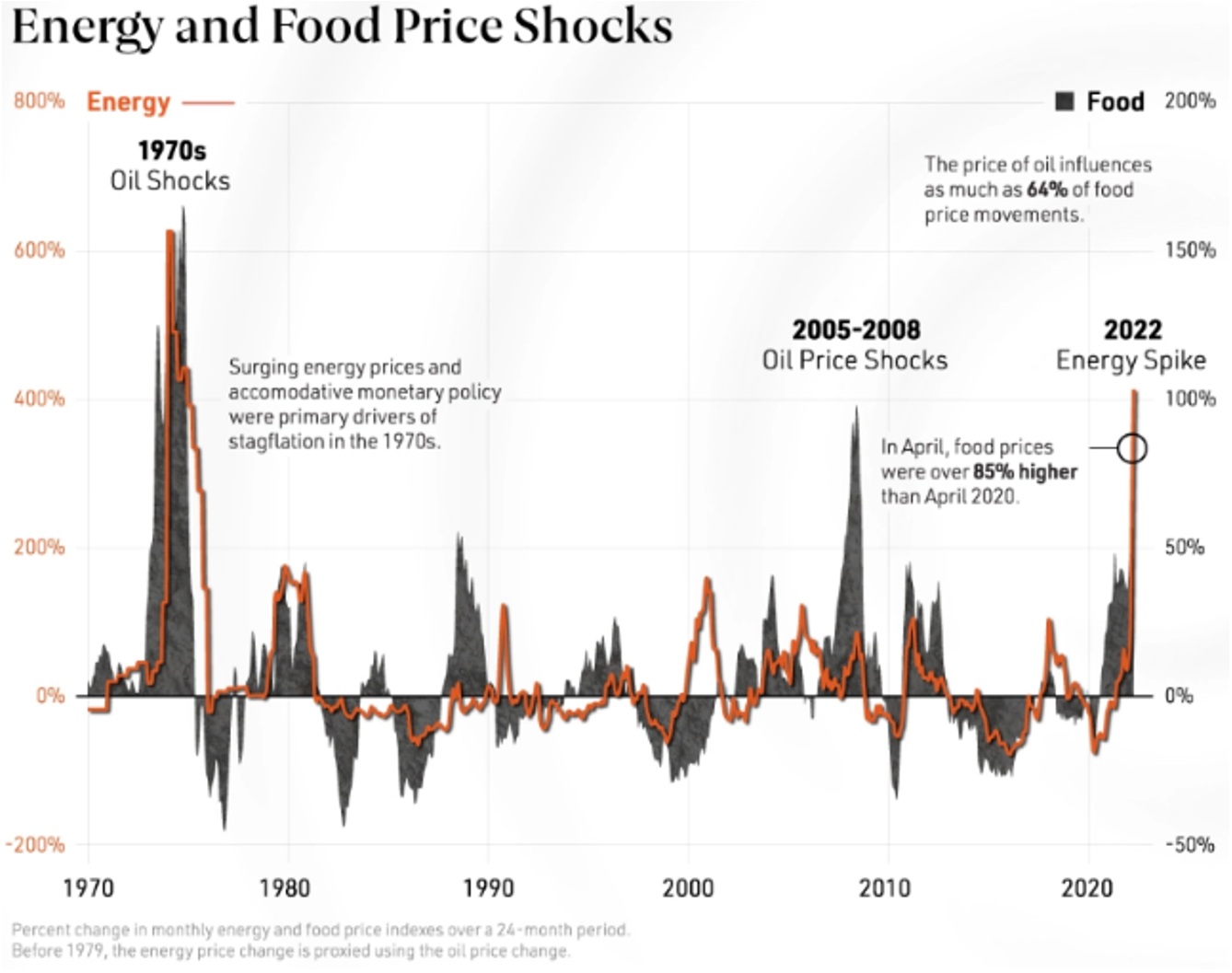

According to survey data published in Oil & Gas Investor[9], approximately 87% of 30 of the largest public oil and gas E&P companies surveyed had an active hedging strategy going into 2022 Energy prices impact a wide variety of economic indicators, including inflationary readings. Energy also directly impacts geopolitical related topics such as global trade and, as seen in the graphic below[10], specifically food security.

We hope that this semi-annual letter serves as a helpful reference to the current market conditions and our approach to investing in private markets. Our team members are always available to answer any questions. Thank you for your continued interest and support.

Sources: [1] Burgiss U.S. Buyout Index, as of June 30, 2022 [2] PitchBook Q3 2022 US PE Breakdown [3]PitchBook Q2 US VC Valuations Report [4] Carta, State of Private Markets: Q2 2022 [5] Q3 2022 PitchBook NVCA Venture Monitor [6] NCREIF, NAREIT, Statista, JP Morgan; Vacancy data as of June 30, 2022; other data based on availability as of August 31, 2022 [7] JPMorgan Q3 2022 Guide to Alternatives [8] U.S. Energy Information Administration; Note: Historical averages: January 7, 1997 – October 18, 2022 [9] Hart Energy July 2022 - Oil and Gas Investor Opportune Hedging Survey [10] Visualcapitalist.com: The Inflation Factor: How Rising Food and Energy Prices Impact the Economy

Important Disclosures

This report shall not constitute an offer to sell, or a solicitation of an offer to buy the interests in Bespoke Private Strategies, LP. No such offer or solicitation will be made prior to the delivery of a definitive private placement memorandum, limited partnership agreement and other materials relating to the matters herein. Before making an investment decision with respect to the fund, potential investors are advised to read carefully the confidential private placement memorandum, the limited partnership agreement and the related subscription documents, and to consult with their tax, legal and financial advisors. An investment in any of these limited partnerships is speculative and involves certain risks and conflicts of interest described in more detail in the private placement memorandum. All investments involve risk including the loss of principal or total loss.

Any indices or other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of dividends and other income and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indices have limitations because indices have volatility and other material characteristics that may differ from a hedge fund. Any indices or other financial benchmarks used herein were not selected to represent an appropriate benchmark to compare an investor’s performance, but rather to allow for comparison of the investor’s performance to that of a well-known and widely recognized index.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Lowe, Brockenbrough & Company, Inc. dba Brockenbrough. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Lowe, Brockenbrough & Company, Inc. is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the Lowe, Brockenbrough & Company, Inc.’s current written disclosure statement discussing our advisory services and fees is available upon request.

The opinions expressed are those of Brockenbrough. The opinions referenced are as of the date of publication and are subject to change due to changes in the market of economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed. Brockenbrough is an investment advisor registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Brockenbrough’s investment advisory services can be found in its Form ADV Part 2, which is available upon request.

Semi-Annual Private Investment Commentary