“Let every man divide his money into three parts, and invest a third in land, a third in business and a third let him keep

in reserve.”

Talmud

(circa 1200BC - 500 AD)

Risk management is a time-honored and time-tested investment principle, as important to achieving investment returns as asset selection. The above quote, written approximately 2,000 years ago, speaks directly to the risk/return trade-off, and is just as applicable today in mitigating investment risk as it was back then. The 67% allocation to risk assets (land and business) and 33% allocation to more stable assets (reserves) is essentially no different than the balanced asset allocations espoused by many of today’s professional investment managers. Of course, the math behind risk management had not been proven 2,000 years ago – adherents only learned from experience.

It wasn’t until the 1950’s and 60’s that the guiding principles of modern portfolio and risk management began to evolve, beginning with the pioneering work of Nobel laureates Harry Markowitz and Bill Sharpe. Markowitz demonstrated that a portfolio’s expected return could be enhanced for a given amount of portfolio risk or, conversely, a portfolio’s risk could be reduced for a given level of expected return, by carefully choosing the proportions of various assets. Meanwhile, Sharpe and others developed a model to explain the relationship between an asset’s market risk (risk that cannot be diversified away) and its expected return, and established a simple method of measuring expected return per unit of risk (Sharpe Ratio). Today, these principles are integral to the practice of portfolio management and help explain why diversification and asset allocation are critical strategies for mitigating investment risk.

But what is investment risk? Commonly defined, risk is the deviation from an expected outcome. Risk is typically measured in absolute terms by standard deviation (see Appendix), or relative to some comparative market benchmark using the concept of beta (see Appendix). And how is risk reduced? Since multi-asset portfolios are less risky than single asset portfolios, portfolio risk is reduced by diversifying investments among various assets with low correlations (see Appendix) to one another, i.e., the assets typically don’t move in lock-step with one another given market-moving events. These strategies are applied not only to equity portfolios, but in allocating among asset classes as well.

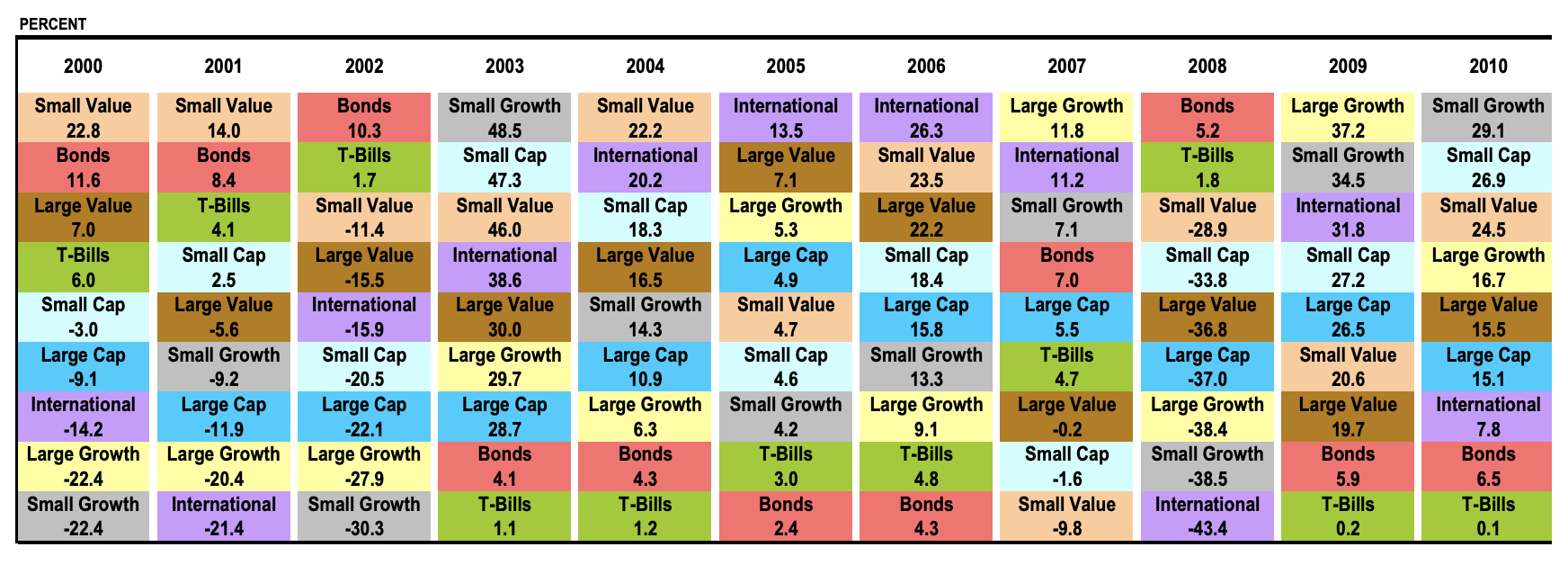

Broadly speaking, there are two types of investment risk; asset-specific risk and market risk. Diversification among equities (a single asset class) reduces asset-specific risk - the risk associated with a particular company, industry, economic sector, country or global region. The chart below shows the variability of equity sector returns over the last 10 years, perfectly illustrating the benefits of allocating among various equity sectors. That is why broadly diversified equity portfolios typically include allocations to domestic large, mid and small cap stocks, growth and value allocations, as well as to developed international and emerging market sectors.

And, though diversifying among various equity sectors helps to mitigate asset-specific risk, it does not address market risk, often referred to as undiversifiable risk.

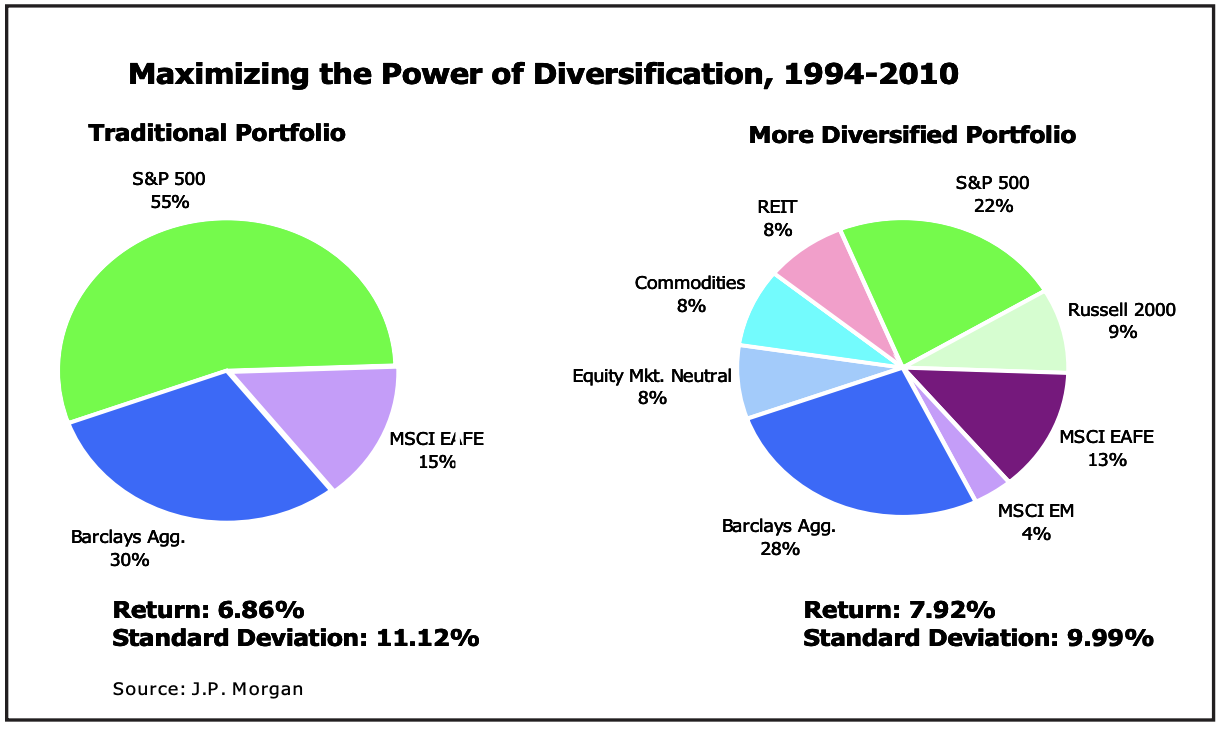

Diversification among various asset classes, or asset allocation, is a broader strategy for mitigating the market risk of being exposed to any one asset class. It is also one of the most critical elements of effective portfolio management, as numerous studies have shown that the asset allocation decision explains up to 90% of investment returns. Of course, the risk/return profile and investment returns of an investor’s portfolio will also be determined by the portfolio’s asset allocation mix, which is a function of the investor’s objectives, risk tolerance and investment time horizon. By investing in multiple asset classes with low correlations to one another, the market risks of any one asset class within the portfolio can be reduced. Historically, asset allocation decisions have been made among more traditional asset classes (stocks, bonds and cash) due to the fact that bonds and cash have very low correlations to stocks. However, by adding additional asset classes to the allocation mix, even greater diversification benefits can be derived in the form of enhanced returns with lower standard deviation, as seen in the charts to the right.

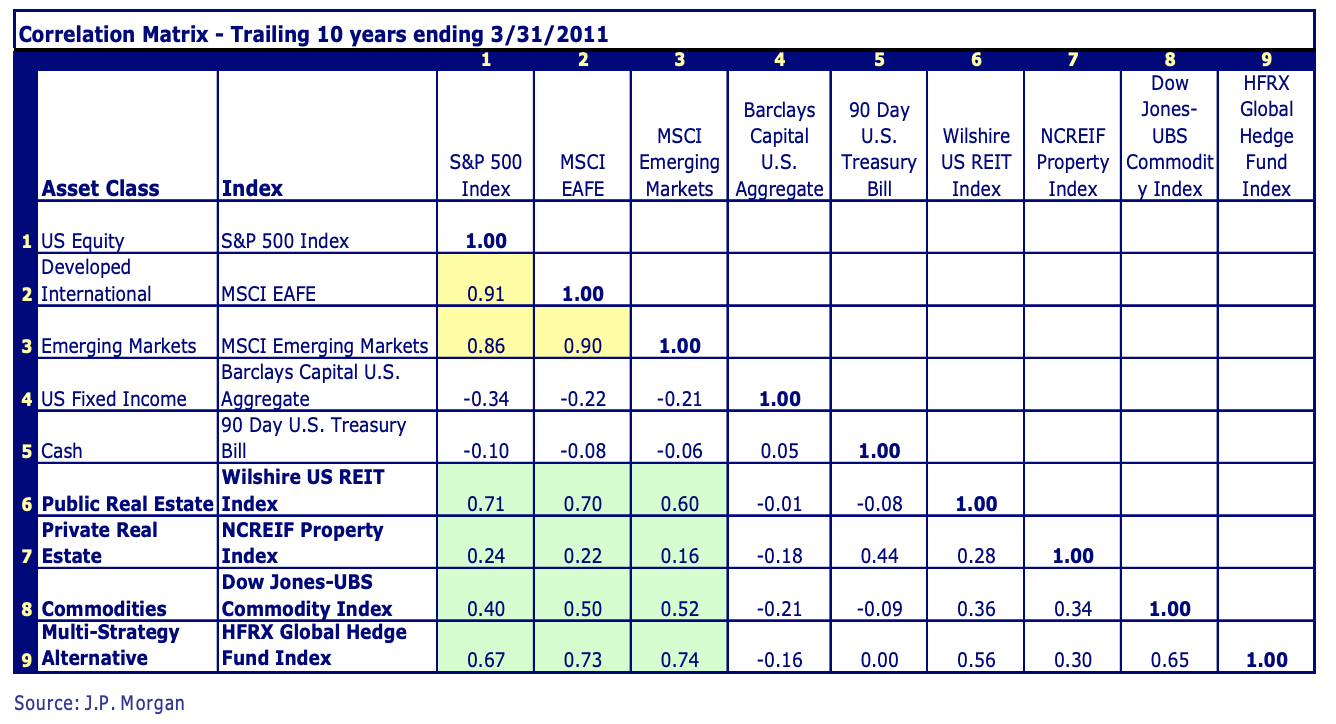

Real estate has proven to be an excellent portfolio diversifier over time (see opening quote) because of its low correlation to equities, despite the collapse of the housing bubble in 2008-09. Additional diversification opportunities exist by investing in other alternative assets. Alternatives encompass multiple asset classes (commodities, real estate, currencies, derivatives, managed futures) and hedging strategies (market neutral, absolute return, merger arbitrage, global macro), but all share a common trait of having low correlations with both equity and fixed income markets, thereby making them ideal portfolio diversifiers for reducing market risk and return volatility, while enhancing returns. The chart right illustrates the low correlation of alternative investments relative to more traditional asset classes. Note the high correlation among the three equity asset classes (in yellow), versus the lower correlations between the highlighted alternative strategies and traditional equity and fixed income asset classes (in green).

Access to these various alternative strategies had, until recently, only been available to large institutional and individual investors due to high investment minimums and fees, and poor liquidity. Over the last few years, the investment management industry has taken advantage of an explosion of more accessible and liquid alternative investment vehicles (mutual funds, exchange-traded funds, exchange-traded notes) to further diversify portfolio risk.

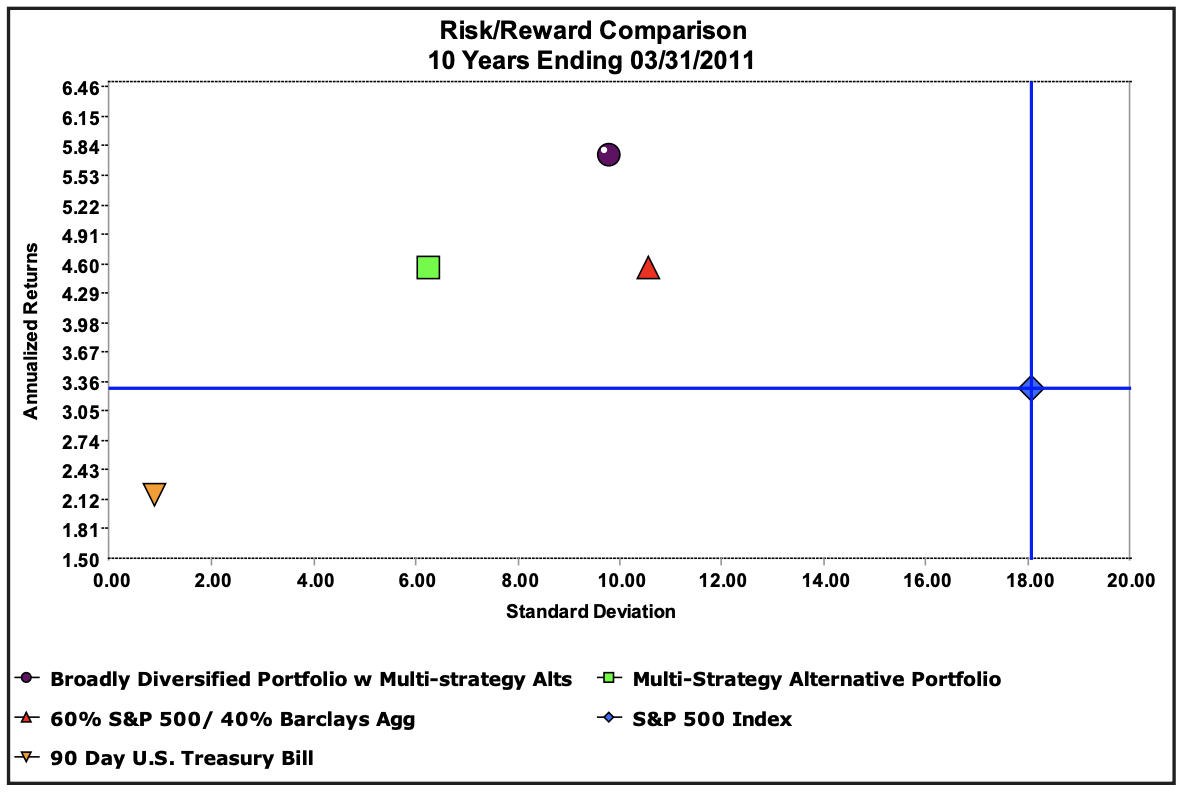

It should be pointed out that, during equity bull markets, inclusion of alternative investments as a diversification strategy will likely dampen return opportunities relative to equity-only strategies. However, it is during bear markets that these alternative strategies provide the greatest risk-adjusted return benefits. The chart below summarizes the risk/return characteristics of several diversified strategies relative to the S&P 500 during the ten year period ended 3/31/2011, which includes both bull and bear markets.

The benefits of diversification among multiple asset classes are powerful, both in terms of the potential for enhanced returns, but equally important for the ability to reduce the volatility of those returns. Given the myriad economic and geopolitical headwinds global markets are currently facing, investors should review their investment portfolios to ensure that their asset allocation strategy not only addresses their own investment objectives and risk tolerances, but also takes advantage of the expanding investment opportunities available by considering multiple asset classes.

Appendix

Beta - the volatility of a security (or portfolio) relative to the market as a whole. The market has a beta of 1.0. An asset with a beta of 1.0 indicates that its price will move with the market. A beta of less than 1.0 indicates lower volatility than the market, with a beta greater than 1.0 indicating greater volatility than the market. For example, if an asset’s beta is 1.2, it is theoretically 20% more volatile than the market.

Correlation - statistical measure that describes on a scale of +1 to -1 the relative price movement of two assets or indices, with +1 indicating perfect positive correlation (assets moving in lockstep with one another), -1 indicating perfect negative correlation, and 0 indicating no correlation at all between price movements.

Standard Deviation - the return dispersion around a central tendency, or mean. In statistics, a 1 standard deviation dispersion from the mean encompasses about 68% of occurrences, while a 2 standard deviation event will occur 95% of the time. So, for example, a stock (or portfolio) with an annualized return (mean) of 7% and a standard deviation of 11% will have a return dispersion of +/-11% around the 7% mean 68% of the time, and a return dispersion of +/-22% around the mean 95% of the time

Diversification, Asset Allocation and the Case for Alternatives