The beatings continued in the third quarter with the S&P 500 and the bond market both down nearly 5%. Small caps fared a bit better, down only 2%, but year-to-date they’re down 25%, slightly worse than large caps. And the broadest measure of bond returns was down a dispiriting 15%. Morale has not improved.

We’re paying the price for fiscal and monetary stimulus run amok – an overdose. In simple terms, way too much money was injected into the system. According to respected hedge fund manager, Paul Tudor Jones, “Inflation is a bit like toothpaste. Once you get it out of the tube, it’s hard to get back in.” Jones expects the Fed will push us into recession to regain control of prices. By the way, you don’t have to be a billionaire to share this opinion. This is now the consensus view.

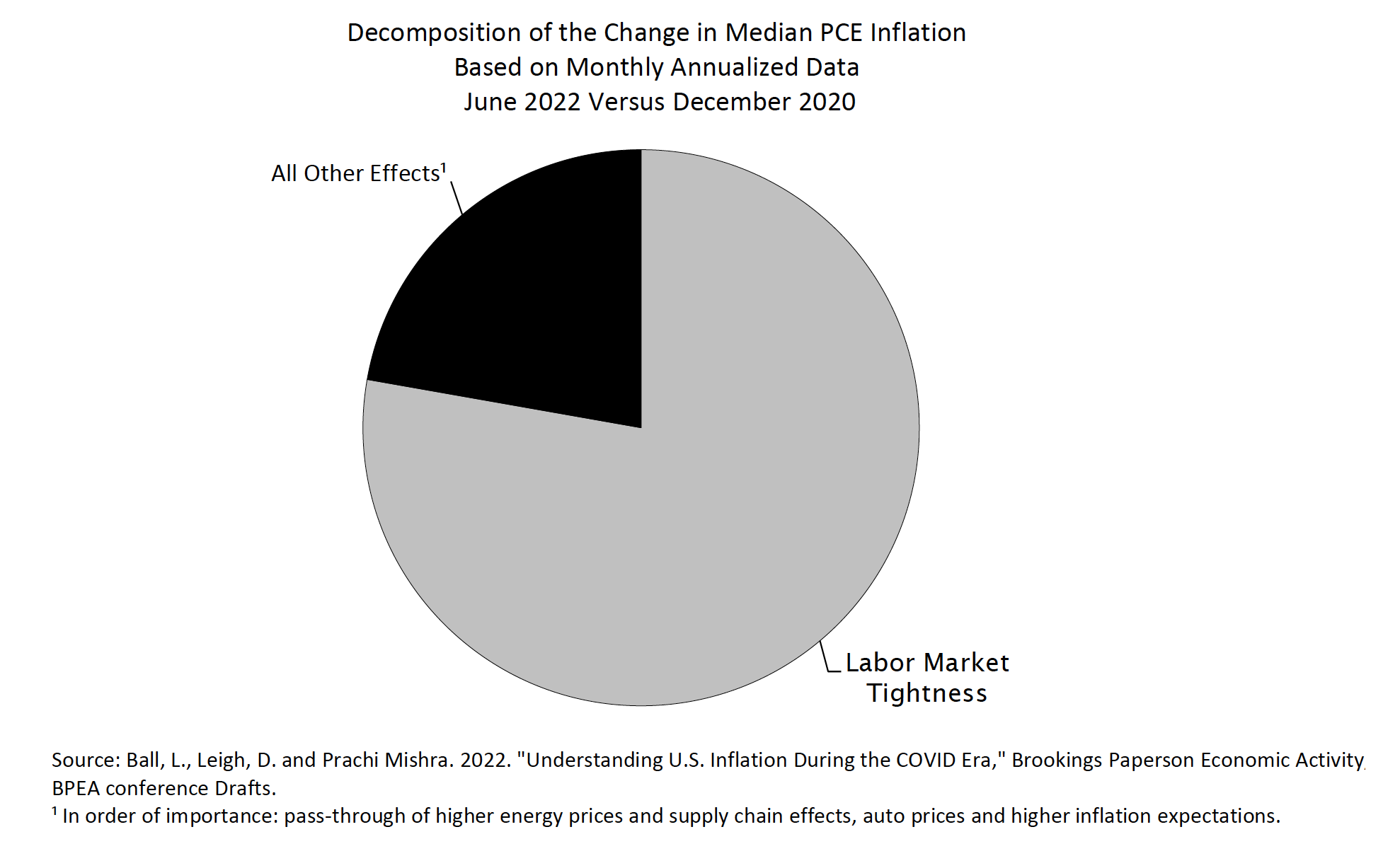

The following chart from Empirical Research illustrates the challenge. We don’t love re-referencing charts, but this one’s important. Energy, commodity and supply chain problems are no longer the main obstacles to lower inflation. A very tight labor market is. Explanations have become politicized…like everything else; but Baby Boomer retirements, long covid and restricted immigration are quantifiably real. The Fed’s extraordinary rate actions will no doubt weaken the economy, but there’s a months-long lag that must be anticipated. This is more art than science, and the Fed has repeatedly failed to anticipate. Too harsh? Honestly, not really. In any case, they will very likely have to see signs of labor market weakness before concluding they’ve done enough. We hope they get their evidence before they break something important.

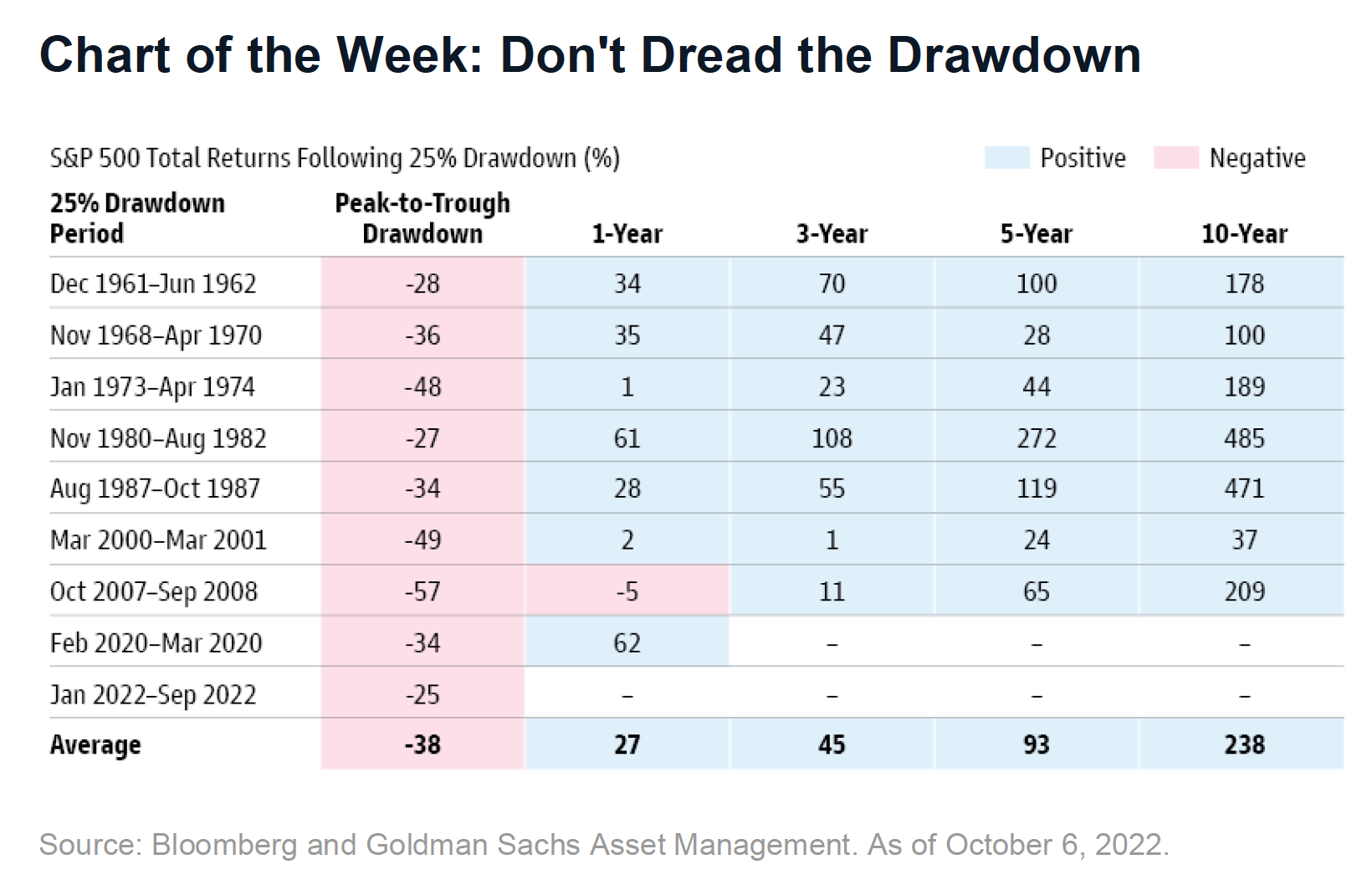

As we’re sure most of you are aware, Brockenbrough is led by eternal optimists. It’s in our nature, but it’s also a demonstrably practical position to take. The following Chart of the Week from Goldman Sachs is illustrative. After the initial 25% decline, the S&P 500 was up from that point one year later in every episode except one. Drawdowns are a fact of life, as are recoveries. That’s 80 years of data encompassing the grimmest of investment predicaments, and we grew out of all of them, no exceptions.

Unhelpfully, there’s no way to know where we are in this drawdown; there could be more. Much will depend upon the coming earnings reporting seasons. We say seasons because employment is currently too strong to conclude the economy is in retreat. But over the next few quarters we may find ourselves there, and the degree of severity of downturn and the durability of margins will play a big role in determining the ultimate outcome. Helpfully, companies are in good shape. Valuations, while not cheap, are fair, and the current composition of the S&P 500 could yield a more resilient margin than in the past.

When writing these quarterlies, we’re gently prodded to get them done in a timely manner, but occasionally we stall a little to gain information, especially when that next news cycle might have us eating crow or something even less appetizing. The first full week of October brought a dramatic two-day rally on weaker economic news followed by a near complete reversal when the September jobs report showed continued employment strength. If the jobs data had been a little weaker, the rally probably would have continued as the market anticipated the end of the Fed rate hike cycle. We throw this in here to highlight the difficulty of timing markets. We don’t know when the employment data will weaken, only that it will. We don’t want to be caught on the sidelines when that happens.

Richard H. Skeppstrom II

Chief Equity Strategist

The opinions expressed are those of Brockenbrough*. The opinions referenced are as of the date of publication and are subject to change due to changes in the market of economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed. Brockenbrough is an investment advisor registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Brockenbrough investment advisory services can be found in its Form ADV Part 2, which is available upon request.

3rd Quarter 2022 Commentary